Estimating Monotonic Effects with brms

Paul Bürkner

2024-03-19

Source:vignettes/brms_monotonic.Rmd

brms_monotonic.RmdIntroduction

This vignette is about monotonic effects, a special way of handling discrete predictors that are on an ordinal or higher scale (Bürkner & Charpentier, in review). A predictor, which we want to model as monotonic (i.e., having a monotonically increasing or decreasing relationship with the response), must either be integer valued or an ordered factor. As opposed to a continuous predictor, predictor categories (or integers) are not assumed to be equidistant with respect to their effect on the response variable. Instead, the distance between adjacent predictor categories (or integers) is estimated from the data and may vary across categories. This is realized by parameterizing as follows: One parameter, \(b\), takes care of the direction and size of the effect similar to an ordinary regression parameter. If the monotonic effect is used in a linear model, \(b\) can be interpreted as the expected average difference between two adjacent categories of the ordinal predictor. An additional parameter vector, \(\zeta\), estimates the normalized distances between consecutive predictor categories which thus defines the shape of the monotonic effect. For a single monotonic predictor, \(x\), the linear predictor term of observation \(n\) looks as follows:

\[\eta_n = b D \sum_{i = 1}^{x_n} \zeta_i\]

The parameter \(b\) can take on any real value, while \(\zeta\) is a simplex, which means that it satisfies \(\zeta_i \in [0,1]\) and \(\sum_{i = 1}^D \zeta_i = 1\) with \(D\) being the number of elements of \(\zeta\). Equivalently, \(D\) is the number of categories (or highest integer in the data) minus 1, since we start counting categories from zero to simplify the notation.

A Simple Monotonic Model

A main application of monotonic effects are ordinal predictors that can be modeled this way without falsely treating them either as continuous or as unordered categorical predictors. In Psychology, for instance, this kind of data is omnipresent in the form of Likert scale items, which are often treated as being continuous for convenience without ever testing this assumption. As an example, suppose we are interested in the relationship of yearly income (in $) and life satisfaction measured on an arbitrary scale from 0 to 100. Usually, people are not asked for the exact income. Instead, they are asked to rank themselves in one of certain classes, say: ‘below 20k’, ‘between 20k and 40k’, ‘between 40k and 100k’ and ‘above 100k’. We use some simulated data for illustration purposes.

income_options <- c("below_20", "20_to_40", "40_to_100", "greater_100")

income <- factor(sample(income_options, 100, TRUE),

levels = income_options, ordered = TRUE)

mean_ls <- c(30, 60, 70, 75)

ls <- mean_ls[income] + rnorm(100, sd = 7)

dat <- data.frame(income, ls)We now proceed with analyzing the data modeling income

as a monotonic effect.

The summary methods yield

summary(fit1) Family: gaussian

Links: mu = identity; sigma = identity

Formula: ls ~ mo(income)

Data: dat (Number of observations: 100)

Draws: 4 chains, each with iter = 2000; warmup = 1000; thin = 1;

total post-warmup draws = 4000

Regression Coefficients:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

Intercept 30.82 1.38 28.07 33.52 1.00 2259 2479

moincome 14.74 0.63 13.49 16.01 1.00 2223 2209

Monotonic Simplex Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

moincome1[1] 0.67 0.04 0.59 0.74 1.00 2110 1960

moincome1[2] 0.26 0.04 0.18 0.34 1.00 3509 2857

moincome1[3] 0.07 0.04 0.01 0.15 1.00 2752 1627

Further Distributional Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

sigma 6.87 0.51 5.97 7.95 1.00 2743 2307

Draws were sampled using sampling(NUTS). For each parameter, Bulk_ESS

and Tail_ESS are effective sample size measures, and Rhat is the potential

scale reduction factor on split chains (at convergence, Rhat = 1).

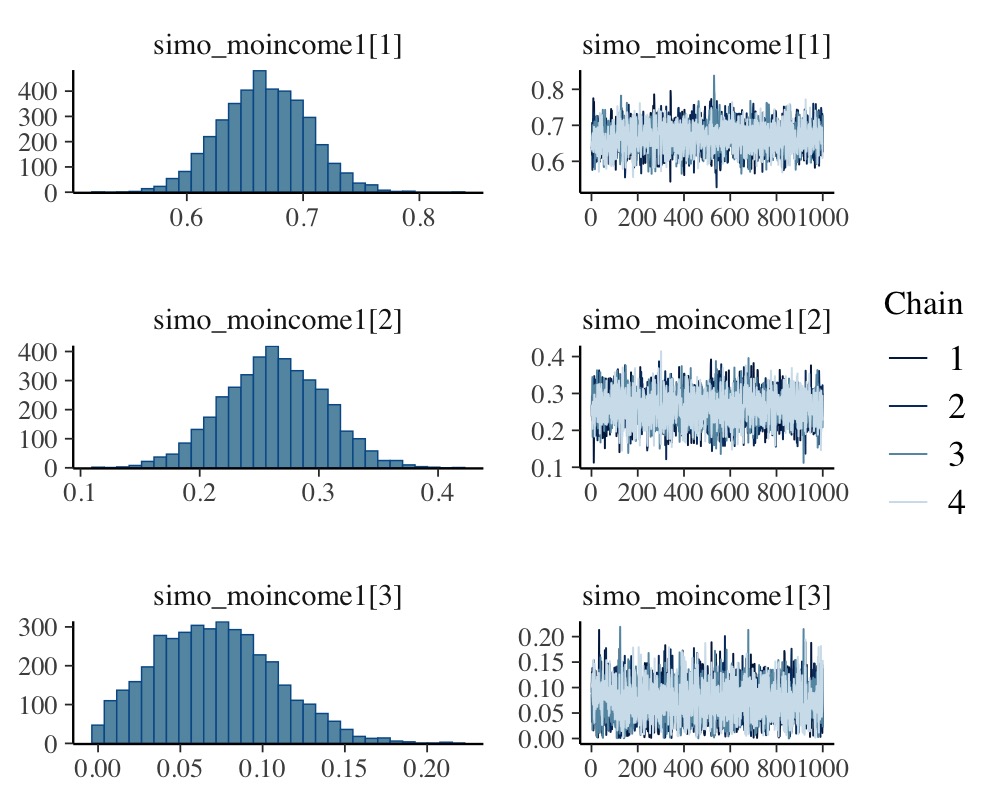

plot(fit1, variable = "simo", regex = TRUE)

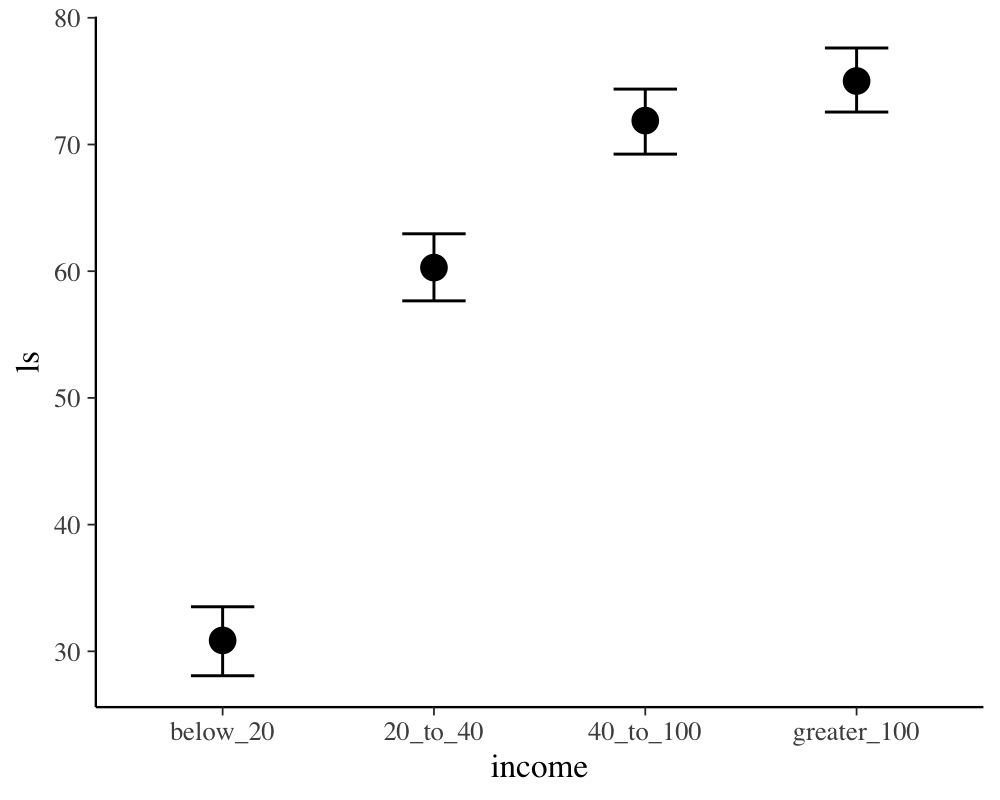

plot(conditional_effects(fit1))

The distributions of the simplex parameter of income, as

shown in the plot method, demonstrate that the largest

difference (about 70% of the difference between minimum and maximum

category) is between the first two categories.

Now, let’s compare of monotonic model with two common alternative

models. (a) Assume income to be continuous:

dat$income_num <- as.numeric(dat$income)

fit2 <- brm(ls ~ income_num, data = dat)

summary(fit2) Family: gaussian

Links: mu = identity; sigma = identity

Formula: ls ~ income_num

Data: dat (Number of observations: 100)

Draws: 4 chains, each with iter = 2000; warmup = 1000; thin = 1;

total post-warmup draws = 4000

Regression Coefficients:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

Intercept 23.91 2.40 19.12 28.64 1.00 3448 2918

income_num 14.36 0.89 12.61 16.09 1.00 3385 2908

Further Distributional Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

sigma 9.72 0.69 8.49 11.17 1.00 3933 2787

Draws were sampled using sampling(NUTS). For each parameter, Bulk_ESS

and Tail_ESS are effective sample size measures, and Rhat is the potential

scale reduction factor on split chains (at convergence, Rhat = 1).or (b) Assume income to be an unordered factor:

contrasts(dat$income) <- contr.treatment(4)

fit3 <- brm(ls ~ income, data = dat)

summary(fit3) Family: gaussian

Links: mu = identity; sigma = identity

Formula: ls ~ income

Data: dat (Number of observations: 100)

Draws: 4 chains, each with iter = 2000; warmup = 1000; thin = 1;

total post-warmup draws = 4000

Regression Coefficients:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

Intercept 30.60 1.40 27.83 33.27 1.00 3147 2789

income2 29.72 1.90 26.01 33.43 1.00 3259 2968

income3 41.49 2.01 37.52 45.45 1.00 3455 2581

income4 44.39 1.97 40.44 48.27 1.00 3534 3110

Further Distributional Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

sigma 6.86 0.51 5.95 7.95 1.00 3840 2689

Draws were sampled using sampling(NUTS). For each parameter, Bulk_ESS

and Tail_ESS are effective sample size measures, and Rhat is the potential

scale reduction factor on split chains (at convergence, Rhat = 1).We can easily compare the fit of the three models using leave-one-out cross-validation.

loo(fit1, fit2, fit3)Output of model 'fit1':

Computed from 4000 by 100 log-likelihood matrix.

Estimate SE

elpd_loo -336.2 7.0

p_loo 4.6 0.8

looic 672.5 13.9

------

MCSE of elpd_loo is 0.0.

MCSE and ESS estimates assume MCMC draws (r_eff in [0.6, 1.1]).

All Pareto k estimates are good (k < 0.7).

See help('pareto-k-diagnostic') for details.

Output of model 'fit2':

Computed from 4000 by 100 log-likelihood matrix.

Estimate SE

elpd_loo -370.1 5.6

p_loo 2.5 0.3

looic 740.2 11.2

------

MCSE of elpd_loo is 0.0.

MCSE and ESS estimates assume MCMC draws (r_eff in [0.8, 1.0]).

All Pareto k estimates are good (k < 0.7).

See help('pareto-k-diagnostic') for details.

Output of model 'fit3':

Computed from 4000 by 100 log-likelihood matrix.

Estimate SE

elpd_loo -336.5 7.1

p_loo 4.8 0.8

looic 672.9 14.1

------

MCSE of elpd_loo is 0.0.

MCSE and ESS estimates assume MCMC draws (r_eff in [0.7, 1.3]).

All Pareto k estimates are good (k < 0.7).

See help('pareto-k-diagnostic') for details.

Model comparisons:

elpd_diff se_diff

fit1 0.0 0.0

fit3 -0.2 0.2

fit2 -33.8 6.7 The monotonic model fits better than the continuous model, which is

not surprising given that the relationship between income

and ls is non-linear. The monotonic and the unordered

factor model have almost identical fit in this example, but this may not

be the case for other data sets.

Setting Prior Distributions

In the previous monotonic model, we have implicitly assumed that all differences between adjacent categories were a-priori the same, or formulated correctly, had the same prior distribution. In the following, we want to show how to change this assumption. The canonical prior distribution of a simplex parameter is the Dirichlet distribution, a multivariate generalization of the beta distribution. It is non-zero for all valid simplexes (i.e., \(\zeta_i \in [0,1]\) and \(\sum_{i = 1}^D \zeta_i = 1\)) and zero otherwise. The Dirichlet prior has a single parameter \(\alpha\) of the same length as \(\zeta\). The higher \(\alpha_i\) the higher the a-priori probability of higher values of \(\zeta_i\). Suppose that, before looking at the data, we expected that the same amount of additional money matters more for people who generally have less money. This translates into a higher a-priori values of \(\zeta_1\) (difference between ‘below_20’ and ‘20_to_40’) and hence into higher values of \(\alpha_1\). We choose \(\alpha_1 = 2\) and \(\alpha_2 = \alpha_3 = 1\), the latter being the default value of \(\alpha\). To fit the model we write:

prior4 <- prior(dirichlet(c(2, 1, 1)), class = "simo", coef = "moincome1")

fit4 <- brm(ls ~ mo(income), data = dat,

prior = prior4, sample_prior = TRUE)The 1 at the end of "moincome1" may appear

strange when first working with monotonic effects. However, it is

necessary as one monotonic term may be associated with multiple simplex

parameters, if interactions of multiple monotonic variables are included

in the model.

summary(fit4) Family: gaussian

Links: mu = identity; sigma = identity

Formula: ls ~ mo(income)

Data: dat (Number of observations: 100)

Draws: 4 chains, each with iter = 2000; warmup = 1000; thin = 1;

total post-warmup draws = 4000

Regression Coefficients:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

Intercept 30.82 1.41 28.00 33.56 1.00 2900 2690

moincome 14.73 0.65 13.44 16.02 1.00 2680 2550

Monotonic Simplex Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

moincome1[1] 0.67 0.04 0.60 0.74 1.00 2559 1907

moincome1[2] 0.26 0.04 0.18 0.35 1.00 3147 2672

moincome1[3] 0.07 0.04 0.01 0.15 1.00 2473 1679

Further Distributional Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

sigma 6.87 0.52 5.95 7.97 1.00 3016 2827

Draws were sampled using sampling(NUTS). For each parameter, Bulk_ESS

and Tail_ESS are effective sample size measures, and Rhat is the potential

scale reduction factor on split chains (at convergence, Rhat = 1).We have used sample_prior = TRUE to also obtain draws

from the prior distribution of simo_moincome1 so that we

can visualized it.

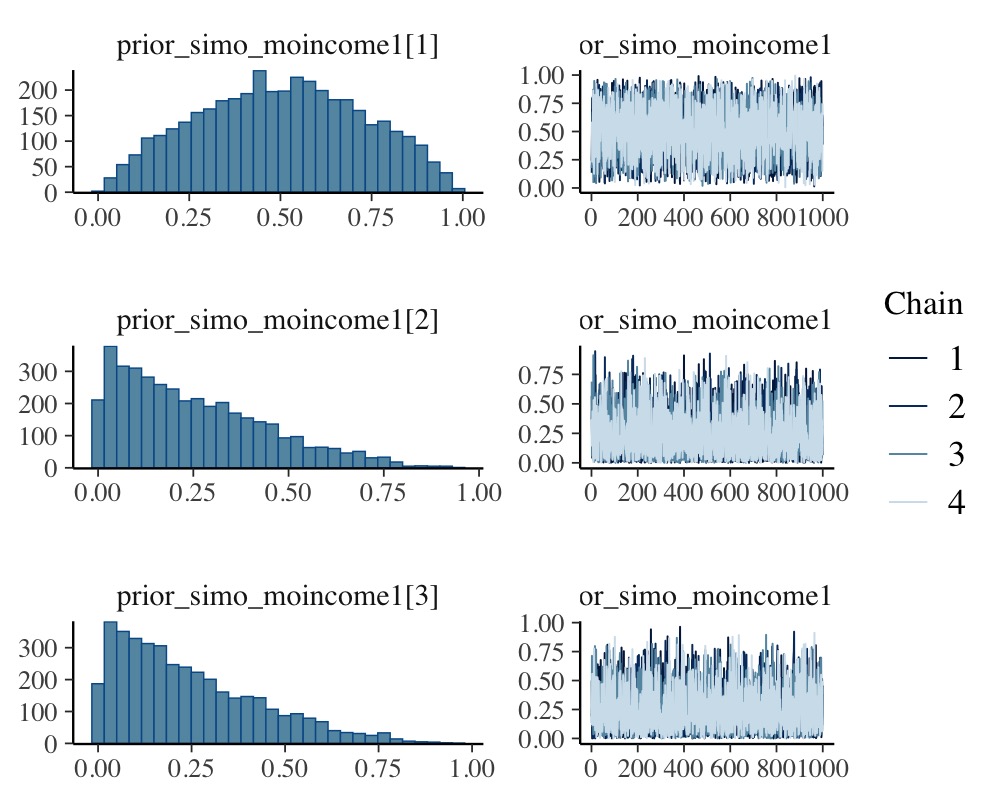

plot(fit4, variable = "prior_simo", regex = TRUE, N = 3)

As is visible in the plots, simo_moincome1[1] was

a-priori on average twice as high as simo_moincome1[2] and

simo_moincome1[3] as a result of setting \(\alpha_1\) to 2.

Modeling interactions of monotonic variables

Suppose, we have additionally asked participants for their age.

dat$age <- rnorm(100, mean = 40, sd = 10)We are not only interested in the main effect of age but also in the

interaction of income and age. Interactions with monotonic variables can

be specified in the usual way using the * operator:

summary(fit5) Family: gaussian

Links: mu = identity; sigma = identity

Formula: ls ~ mo(income) * age

Data: dat (Number of observations: 100)

Draws: 4 chains, each with iter = 2000; warmup = 1000; thin = 1;

total post-warmup draws = 4000

Regression Coefficients:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

Intercept 38.23 6.22 27.32 51.46 1.00 1271 2044

age -0.18 0.15 -0.50 0.08 1.00 1249 1768

moincome 11.31 2.75 5.66 16.32 1.00 1120 2224

moincome:age 0.09 0.07 -0.04 0.23 1.00 1145 2134

Monotonic Simplex Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

moincome1[1] 0.69 0.11 0.46 0.90 1.00 1593 1525

moincome1[2] 0.24 0.10 0.03 0.44 1.00 1677 1729

moincome1[3] 0.07 0.05 0.00 0.19 1.00 2570 1713

moincome:age1[1] 0.47 0.25 0.03 0.90 1.00 1702 2001

moincome:age1[2] 0.33 0.22 0.01 0.82 1.00 2035 2170

moincome:age1[3] 0.20 0.17 0.01 0.67 1.00 1921 2258

Further Distributional Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

sigma 6.84 0.51 5.92 7.92 1.00 3078 2408

Draws were sampled using sampling(NUTS). For each parameter, Bulk_ESS

and Tail_ESS are effective sample size measures, and Rhat is the potential

scale reduction factor on split chains (at convergence, Rhat = 1).

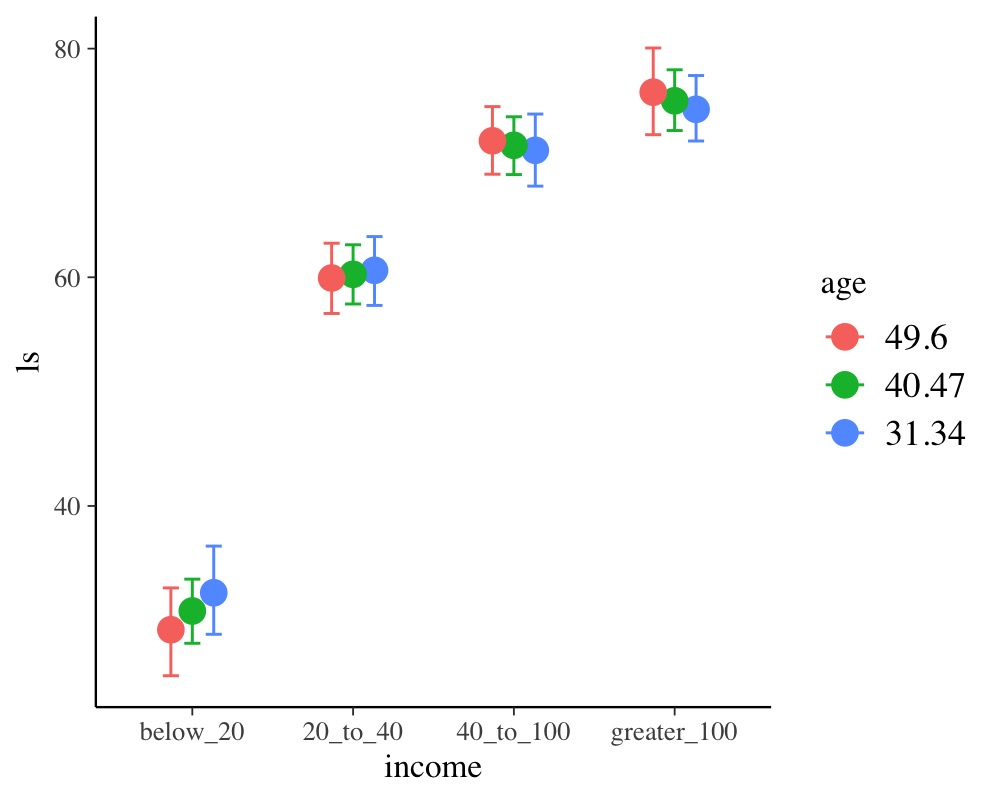

conditional_effects(fit5, "income:age")

Modelling Monotonic Group-Level Effects

Suppose that the 100 people in our sample data were drawn from 10

different cities; 10 people per city. Thus, we add an identifier for

city to the data and add some city-related variation to

ls.

dat$city <- rep(1:10, each = 10)

var_city <- rnorm(10, sd = 10)

dat$ls <- dat$ls + var_city[dat$city]With the following code, we fit a multilevel model assuming the

intercept and the effect of income to vary by city:

summary(fit6) Family: gaussian

Links: mu = identity; sigma = identity

Formula: ls ~ mo(income) * age + (mo(income) | city)

Data: dat (Number of observations: 100)

Draws: 4 chains, each with iter = 2000; warmup = 1000; thin = 1;

total post-warmup draws = 4000

Multilevel Hyperparameters:

~city (Number of levels: 10)

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

sd(Intercept) 12.95 3.78 7.52 21.13 1.00 1210 2249

sd(moincome) 1.56 1.11 0.08 4.22 1.00 938 1982

cor(Intercept,moincome) -0.26 0.46 -0.93 0.80 1.00 2598 1934

Regression Coefficients:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

Intercept 43.42 9.03 26.47 61.52 1.00 1208 1850

age -0.29 0.19 -0.65 0.06 1.00 1214 2517

moincome 9.22 3.43 2.83 15.70 1.00 1194 2199

moincome:age 0.13 0.08 -0.02 0.29 1.00 1186 2272

Monotonic Simplex Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

moincome1[1] 0.58 0.16 0.18 0.84 1.00 1441 1566

moincome1[2] 0.32 0.15 0.06 0.67 1.00 1691 1881

moincome1[3] 0.10 0.08 0.01 0.32 1.00 2076 1937

moincome:age1[1] 0.59 0.23 0.06 0.93 1.00 1596 2033

moincome:age1[2] 0.27 0.19 0.01 0.74 1.00 2203 2364

moincome:age1[3] 0.15 0.15 0.00 0.60 1.00 2305 2108

Further Distributional Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

sigma 6.39 0.52 5.45 7.49 1.00 3000 3133

Draws were sampled using sampling(NUTS). For each parameter, Bulk_ESS

and Tail_ESS are effective sample size measures, and Rhat is the potential

scale reduction factor on split chains (at convergence, Rhat = 1).reveals that the effect of income varies only little

across cities. For the present data, this is not overly surprising given

that, in the data simulations, we assumed income to have

the same effect across cities.

References

Bürkner P. C. & Charpentier, E. (in review). Monotonic Effects: A Principled Approach for Including Ordinal Predictors in Regression Models. PsyArXiv preprint.